By Luke Smith · 7/27/2023

Between major markets in APAC, North America, Europe, and Latin America, nearly 1.7 GW of absorption has occurred in 2023. Pricing volatility and market conditions in 2022 delayed the execution of some large transactions, pushing them to close in 2023 instead. Emerging technologies, like AI, are also driving elevated demand and increasing the sizes of requirements. Demand at the scale seen in the last 12 months is generating a power supply issue in many major markets, resulting in the emergence of new markets and submarkets.

North American Data Center Markets

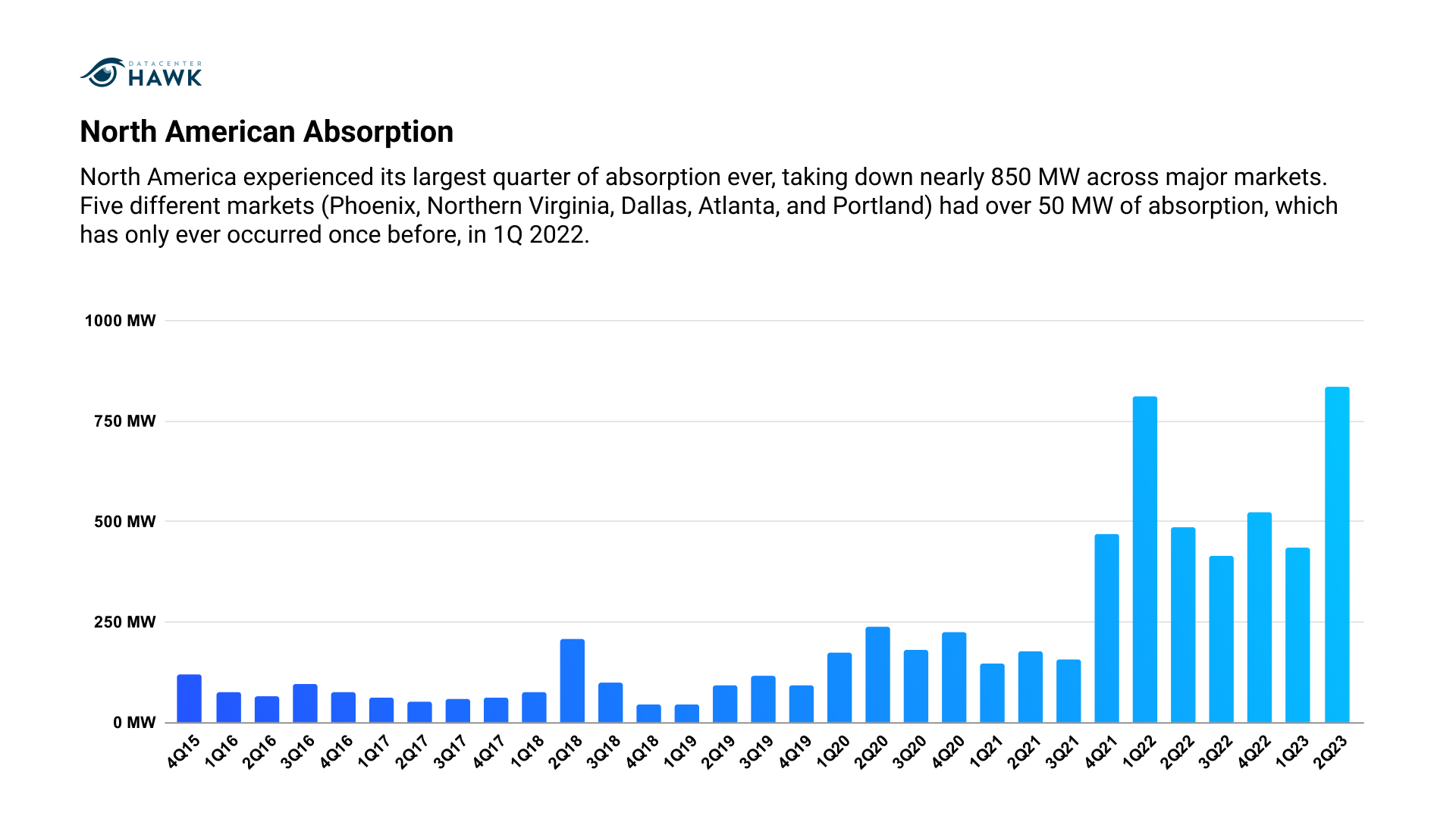

North America experienced its largest quarter of absorption ever, taking down nearly 850 MW across major markets. Five different markets (Phoenix, Northern Virginia, Dallas, Atlanta, and Portland) had over 50 MW of absorption, which has only ever occurred once before, in 1Q 2022. Furthermore, additional requirements are circling the industry, many in emerging markets like Austin, Columbus, Charlotte, and Houston. Elevated demand, a lack of available inventory, long delivery timelines, and a narrow power supply is leading development to occur wherever it can, in major established markets and in new emerging markets.

Notable Trends

AI contributing to major demand in all markets

Among all of the potential game-changers in the industry, AI has quickly become the most material. AI workloads are contributing to current absorption and account for a major portion of incoming RFPs. The compute-heavy nature of these requirements funnels them toward markets with lower power and operating costs. Many deployments are in the 1-5 MW range, however, and are looking at markets like New Jersey, Houston, or Minneapolis where providers have contiguous vacant space suitable to support requirements of that size.

Big quarter for Atlanta and Phoenix

Both Atlanta and Phoenix had record-setting absorption in 2Q 2023. With nearly 100 MW of absorption, Atlanta further established itself as a primary market attractive to hyperscale companies and enterprise users. Despite its scale, Phoenix is one of the fastest-growing markets in North America. Sitting at 295 MW at the end of 2020, Phoenix has grown by over 375% to 1105 MW in 2Q 2023, becoming the second North American market to eclipse 1000 MW. Absorption in Phoenix was also higher than absorption in Northern Virginia in 2Q 2023, at 250 MW.

Requirements getting larger

Although rare five years ago, 36 MW leases are becoming increasingly commonplace. In many markets, 72 MW leases are just as common, and transactions over 100 MW aren’t unheard of. These hyperscale requirements often include entire buildings or campuses. AI deployments are contributing to this increasing requirement size, as AI’s compute-dense deployments require ample power. As a result, providers are building larger data centers with multiple stories, many on massive campuses of 100 acres or more.

Looking Forward

Although absorption was high in 2022, many large transactions were delayed due to pricing volatility. These transactions are now moving forward, contributing to the record-breaking absorption that occurred in 2Q 2023. Hyperscale demand isn’t going to decline but will run into a bottle-neck as a growing number of markets encounter power supply. This will continue to drive pricing upward and create opportunities in emerging markets across North America.

Latin American Data Center Markets

As of today, Latin America has an inventory of 675 MW of power distributed throughout the various data centers in the region. The top five markets-Sao Paulo, Queretaro, Santiago, Bogota, and Mexico City, make up 505 MW or 74 % of the available capacity. Sao Paulo continues to be the market leader with 256 MW, but a 5X planned growth for Queretaro based on current construction projects and announcements could even out these two markets in the next five years. The next emerging market in the region based on market size and potential is Bogota, where 130 MW of projects have been announced, a 4X of current inventory as they anticipate hyperscale deployments. Still, until now, there has been very little construction activity to capture this demand.

The “hyperscale wave” to Latin America is also attracting investments in new submarine cable projects to improve the latency between regions significantly. It will be a significant contributor to the data center expansions. New cable systems connecting the region to Australia and Portugal without transiting via the U.S. are being announced and deployed intra-regional capacity between Brazil and Argentina that will double the capacity between these two countries; and a new system connecting the Yucatan Peninsula and Miami via the Gulf of Mexico will significantly reduce latency to the East coast and Europe from Mexico City.

Notable Trends

Major cloud providers bolstering their presence in Latin America with local deployments

Reliable, local, and low-latency cloud access continues to drive the Latin American data center market, especially in markets like Queretaro, Sao Paulo, and Santiago. AWS announced the implementation of local zones in several cities - placing AWS compute, storage, and other selected services closer to large population centers. Microsoft is completing the construction of three data centers in Queretaro to launch their second Azure cloud region in Latin America called Mexico Central Region, with three availability zones. Oracle, who has been offering their OCI services in Queretaro for more than a year, announced that they would be expanding OCI access to Monterey, Mexico, which aligns with the tremendous growth in Northern Mexico from foreign direct investments to support the exploding “near-shoring” growth.

Influx of new capacity into Latin America creating opportunity for new development

There is a substantial flow of capital into the LATAM data center market from different infrastructure funds looking to capitalize on this growth. Macquarie Group and Actis closed deals to invest in GTD out of Chile and Nabiax. At the same time, I Squared Capital, Stonepeak, Digital Bridge, and Brookfield Infrastructure continue to support the funding for expansions for KIO, Cirion, Scala, and Ascenty.

Looking Forward

Latin America still needs to catch up to the rest of the developed world regarding digital infrastructure but has some of the largest population centers and digital demands. There is a tremendous capital influx and construction in the primary markets. Still, rising land values, energy supply shortage, and supply chain delays impact specific Latin American markets and must be addressed to sustain this growth. Absorption rates have increased as construction projects are completed, and pre-leases are signed. Current construction and planned capacity data show a 2.3X growth for the five primary markets by 2025.

European Data Center Markets

For the last two years, the FLAPD markets have consistently absorbed approximately an average 150 MW of combined absorption per quarter. The consistency in absorption is often a result of power supply and regulations in major markets, limiting absorption to markets that can accommodate requirements at that time.

Notable Trends & Markets

Development broadening geographically

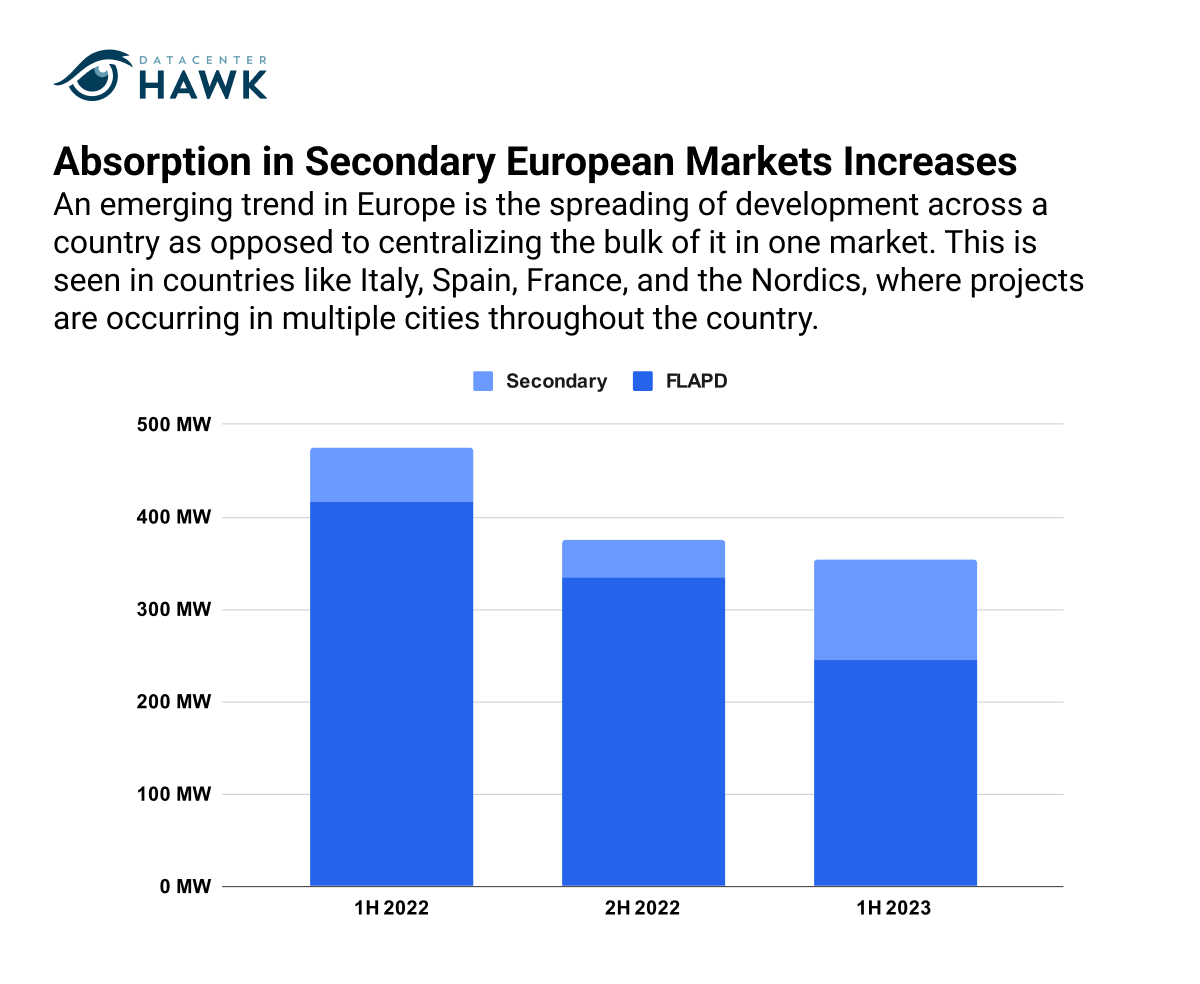

An emerging trend in Europe is the spreading of development across a country as opposed to centralizing the bulk of it in one market. Although primary markets will continue to receive investment, connectivity and power supply limitations are driving geographic diversity. This is seen in countries like Italy, Spain, France, and the Nordics, where projects are occurring in multiple cities throughout the country.

Hyperscale demand occurring in all markets

Demand for hyperscale data center capacity is widespread in Europe. While absorption in FLAPD markets was consistent, over 100 MW of absorption has occurred in secondary European markets through the first half of 2023. Additional requirements are evaluating these secondary markets, which will contribute to elevated absorption through the end of the year.

Multiple new projects bolstering planned capacity in the Nordics

Development limitations in major European markets is pushing more development to the Nordics. The region’s planned power has grown by approximately 34% within the last 12 months. Helsinki is the largest contributor to the region’s growth, with over 140 MW of new projects announced in the market in 2023 despite being one of the smallest emerging European markets by total size.

Looking Forward

Like North America, demand is increasing in Europe, particularly from hyperscale companies and AI requirements. Absorption in each market will be inconsistent, occurring heavily when power is available and lighter when it’s not. While this was common in FLAPD markets, this is now the situation in many secondary markets as well.

Asia-Pacific Data Center Markets

Hong Kong, Singapore, and Sydney combined for over 50 MW of absorption in 2Q 2023, the highest since 1Q 2022. Hong Kong and Singapore are both markets with little vacant supply or room for future growth. Interest in the APAC region as a whole remains high, with consistent development and new capital frequently invested.

Notable Trends & Markets

New supply coming in historically limited markets

As stated above, Hong Kong and Singapore are constrained markets with long development timelines, limited power, and few large parcels suitable for data center development, contributing to relatively flat growth in recent years. For these reasons, Singapore enacted a moratorium on data center development in 2019. Although it has since been lifted, development has been slow, and planned power has declined substantially leaving a handful of projects remaining. In 2Q 2023, however, Singapore approved 80 MW of new data center projects that can begin development in the near future.

Data sovereignty keeping driving demand and keeping absorption with domestic providers

APAC companies often prefer to keep their business with domestic data center providers, due to familiarity and with the aim of preserving data sovereignty. As a result, it can be more complicated to international providers to gain a foothold in the region. Furthermore, hyperscale companies are choosing to build their own campuses instead of leasing from providers, limiting large-scale absorption.

Looking Forward

With new capacity coming online, there will be an uptick in absorption in major APAC markets in the coming years. High rental rates and limited supply will likely keep most large-scale development out of major markets, though absorption will be consistent. Other emerging regions like Johor, Kuala Lumpur, and markets in Australia, among others, will benefit from large-scale development.